Winners and Losers from the “Cost of Living Crisis”

Hi Everyone,

With any crisis there are always winners and losers. In this post, I discuss the likely winners and losers from the current “cost of living crisis”. For additional perspective, I also explore the typical winners and losers from economic crises in general. Investigating the potential winners and losers is a useful exercise. It provides insight into how and why some people and businesses are better positioned to survive or even thrive during and/or immediately after the crisis. It may also shed some light on the events that led up to the crisis as well the responses during the crisis.

I have written a few posts about winners and losers. These include the Governments’ responses to Covid-19 and war in the context of the war in Ukraine (Part 1 and Part 2). These posts are relevant to the current crisis and add perspective to some of the discussions in this post.

The occurrence of the “cost of living crisis” is closely linked to Governments’ responses to Covid-19 and the war in Ukraine. However, the root causes go much deeper than current events. This is explained in my post Cost of Living Crisis – A Collection of Symptoms caused by Serious Long-term Political Failure. The “cost of living crisis” has been by design and is not a natural part of the business cycle. Therefore, the winners and some losers would have been predetermined rather than through their own natural response to the crisis.

Recessions are a naturally occurring part of the business cycle (demand-side)

Economies follow natural cycles of booms (strong growth) and busts (stagnant and negative growth). The business cycle relates to business success but it also impacts people as unemployment increases (people lose their jobs). Typically during a recession, demand for goods and services fall. This drop could occur for any number of reasons. This is often because demand was unsustainably high or a source of demand has been reduced or lost. This could be demand from people, businesses, Government, or exports. As demand falls, business revenues fall. Businesses that provide goods and services that people feel they can live without tend to suffer more. Businesses, if they believe that demand is going to continue to fall or not bounce back soon, may attempt to reduce costs so as to maintain a profit or reduce losses. Cost reductions often involve releasing some employees. Unemployment increases; this further reduces demand. This creates a downward spiral.

Recessions appear bad because they cause hardship to some. However, they are often necessary. Continuous growth and prosperity weakens the economy and society as the standard to succeed is lowered. Recessions require people and businesses to find a way to succeed. Therefore, strengthens them and ensures that prosperous times will return. Hence, the cycle continues. An absence of recessions would eventually lead to prolonged stagnation masked by the illusion of growth supported by debt. An economic collapse would be inevitable and would be far more severe than any cyclical recession.

Who would we normally expect to be the winners and losers of an economic crisis?

Winners and losers of an economic crisis are determined by the causes of the economic crisis (e.g. demand side, supply side, or both) and by the type of Government intervention and the extent of this intervention. Economic crises are expected to be recessions caused on the demand-side. Government and Central Banks have predetermined responses to these types of recessions. They are expansionary fiscal and monetary policies respectively. This section briefly discusses the winners and losers based on strong active and minimal or no intervention.

With strong active intervention

Governments often intervene by increasing Government expenditure and/or lowering taxes (i.e. expansionary fiscal policy) in an attempt to stimulate demand. Central Banks lower interest rates (i.e. expansionary monetary policy) to encourage investment and borrowing. Intervention hastens the recovery of the economy. In most cases, these approaches mitigates most of the short-term problems. Under these circumstances, we can expect the following to be short-term winners or have avoided being losers in the absence of intervention.

- Businesses with deep pockets (financial reserves).

- Businesses providing essential goods and services.

- People who work for businesses who provide essential goods and services.

- People who are able to justify remaining employed.

- Businesses that survive because of Government intervention.

- Government for taking actions to prevent a long recession.

There will still be some short-term losers but it will appear to be minimised because of the reasonably quick recovery. In the long-term, the economy and society are greatly harmed. The recession has not fulfilled an important role of enabling firms to adapt to changing circumstances while eliminating the ones that cannot. Future recessions are likely to be more serious. This is of little concern to Governments as they are more focused on maintaining current popularity than long-run prosperity. Hence, strong active intervention is the typical Government approach.

With minimal or no intervention

In the absence of intervention, the economy can recover. It will take longer and will be harsher as the spiral will continue until the market responds. It is difficult to predict the duration of this recovery. However, the recovery in the long-run could be stronger as the strongest and most innovative businesses will have the best chances of surviving (e.g. Darwinian approach to business) and will eventual thrive. This will cause demand to increase, which will stimulate investment and growth, which will reduce unemployment, which will lead to the start of another boom. Below are likely winners.

- Business that are able to innovate to reduce costs and/or maintain demand.

- Businesses that are flexible and able to adapt to changes in demand.

- Businesses that are able to find or create new markets for their products

- People with essential skills sets.

- People with adaptable and flexible skill sets.

There will be many losers. Small businesses that cannot respond quickly will fail. Larger businesses that survive because of their financial reserves may struggle to thrive if they are unable to adjust to new innovative competitors. People are unable to change or upgrade their skills to suit the new environment may struggle for a long time to regain employment.

This economic crisis is different

So far, I have discussed recessions that are part of the business cycle, which are normally demand driven. The “Cost of Living Crisis” is not demand driven. It could be considered supply driven but should be more accurately called intervention driven. The crisis is a combination of high inflation and stagnant or negative economic growth. Unemployment is at or close to record lows for many western countries. However, if economies continue to stagnate, businesses will start to struggle. They may fail or need to release employees thus causing unemployment to rise. At this point, most of the world could be in a serious stagflation recession. I imagine we will need a new term to describe it.

The “Cost of Living Crisis” did not begin in 2022. It did not even begin in 2020 with the responses to Covid-19. However, the responses to Covid-19 was the trigger for unleashing the symptoms of decades of bad economic policy. Therefore, for the purpose of this post, the winners and losers of the “Cost of Living Crisis” are identified based on the manifestation of the symptoms of the crisis.

Winners

Despite the hardship most people will suffer, there will be some people and businesses who will be considerably better off. This might occur immediately for some and for others they may appear initially worse off but are being positioned to be significantly better off once the crisis has ended or moved onto another stage. There are several indications that this is occurring.

I have grouped who I believe to be the likely winners into 8 groups. These are as follows.

- Big Business

- Banks

- Media

- Government (discussed in conclusion)

- Religion

- US Establishment

- China’s Establishment

- Global Establishment

Big Business

Big businesses such as pharmaceutical companies, weapons manufacturers, oil companies, the largest retailers and many other large businesses have greatly profited since the start of the crisis. This section considers profits, revenue, and share prices of some the largest businesses in the world in their respective sectors (mostly based in the USA).

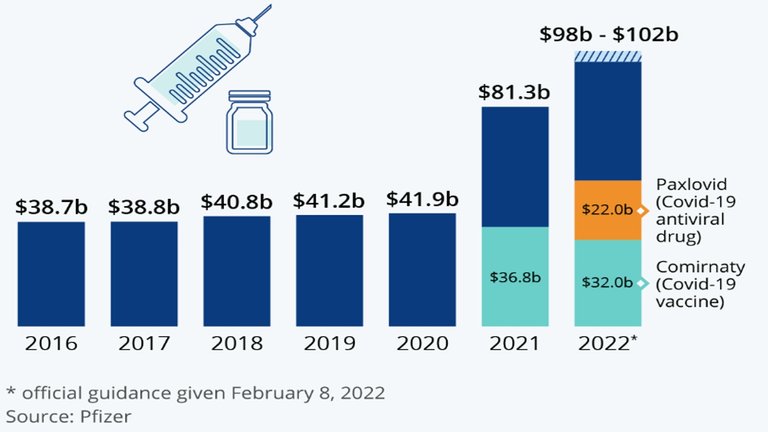

Below are the profits or change in share price of several major pharmaceutical companies.

Figure 1: Pfizer’s Annual Revenue (2016 to 2022 projected)

Source: Statista

Figure 2: The Impact of Vaccines on Pharmaceutical Profits

Source: Statista

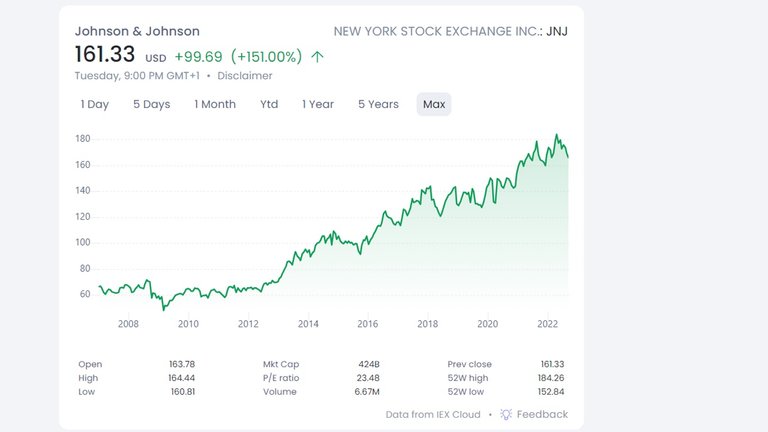

Figure 3: Johnson and Johnson Share Price (2007 to 2022)

Source: IEX Cloud

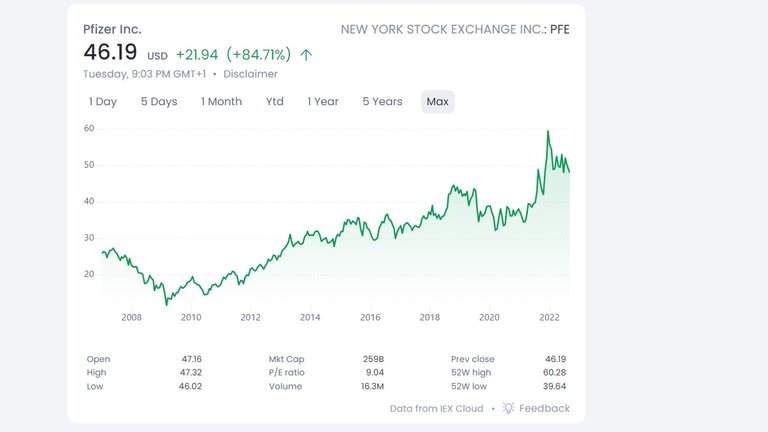

Figure 4: Pfizer Share Price (2007 to 2022)

Source: IEX Cloud

Pharmaceutical companies have greatly profited from the development and sale of Covid-19 jabs to Governments. The jump in profits began in 2021 when they became widely distributed in most western countries. Profits continue to be maintained into 2022 with the sale of booster jabs and for Pfizer the anti-viral drug Paxlovid. Pharmaceutical companies will not be negatively affected by the “Cost of Living Crisis”. Below are some of the possible reasons.

- They do not depend on market forces for demand.

- Their jabs are ineffective at preventing the spread of Covid-19 or preventing serious illness. Therefore, regular boosters are claimed to be needed.

- Their jabs have serious side effects for potentially millions of people. This potentially broadens their market for the sale of other treatments.

- Healthcare has inelastic demand as it is considered a necessity.

The success of most pharmaceutical companies is based on crony capitalism. The Covid-19 jabs are examples of products that have profited them mostly because they do not work.

Figure 5 contains the changes in share price of Lockheed Martin (World’s Largest Supplier of Weapons) in 2021/22

Figure 5: Lockheed Martin Share Price (World’s Largest Supplier of Weapons) in 2021/22

Source: IEX Cloud

The moment the war began in Ukraine, the share price of Lockheed Martin jumped by about 20%. It has continued to remain high and will not be affected by the “Cost of Living Crisis”. Western countries are flooding Ukraine with weapons. More weapons will be built to continue the supply to Ukraine as well as new ones to replace the ones that have already been sent. Large weapons companies like Lockheed Martin are protected from the crisis as they are supported by Government expenditure and do not need to rely on market forces.

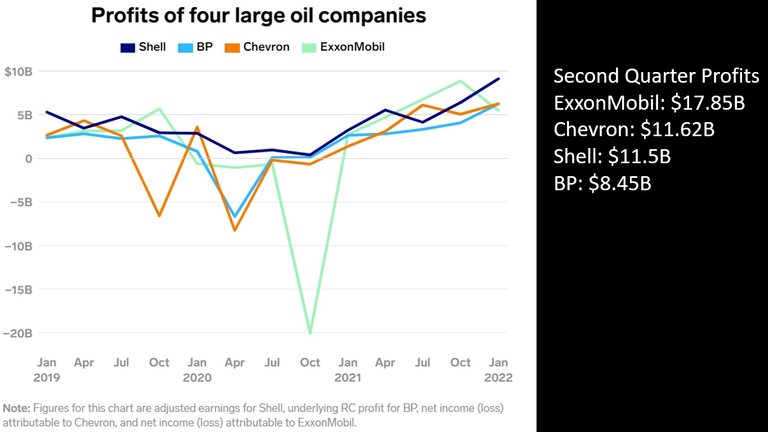

Figure 6 contains profits of the four largest Oil Companies from January 2021 to the second quarter of 2022.

Figure 6: Profits of Four Largest Oil Companies (January 2021 to second Quarter 2022)

Sources: Data 2019 to January 2022 Business Insider, second quarter 2022 data for Exxon and Chevron cited by The Guardian second quarter 2022 data for Shell cited by The Guardian, and second quarter 2022 data for BP cited by Fortune

The war in Ukraine is the second part of the trigger for the “Cost of Living Crisis”. The extensive amount of money and weapons being sent to the Ukraine is draining the resources of many western countries but the sanctions are triggering the high costs of oil and gas. Oil and gas companies are taking advantage of these high costs to vastly increase their profits. If the prices continue to increase, many people will not be able to afford petrol for their cars or energy to heat their homes in the winter.

Governments are intervening by placing energy caps and guarantees so that energy prices will not continue their spiralling upward trend (Independent).This will also ensure that oil and gas companies can continue making excessively high profits with less fear that their customers will not be able to pay. UK has also lifted the ban on fracking as a response to their own sanctions on Russia (Euronews). This is also likely to provide another lucrative stream of revenue to several of the major oil and gas companies.

Figures 7 and 8 contain net revenue and sales for Walmart and Amazon.

Figure 7: Net Sales of Walmart in Billions US$ (2006 to 2022)

Source: Statista

Figure 8: Net Revenue of Amazon in Billions US$ (2004 to 2022)

Source: Repricerexpress

Walmart and Amazon are the two largest retailers worldwide. Neither of their sales were negatively affected during the 2008 financial crisis, the Covid-19 closures, and apparently not as the “Cost of Living Crisis” hits with full force. Sale of goods with inelastic demand and their ability to avoid the impact of restrictions (e.g. ability to operate online) has enabled these businesses to succeed regardless of how the economy looks in general.

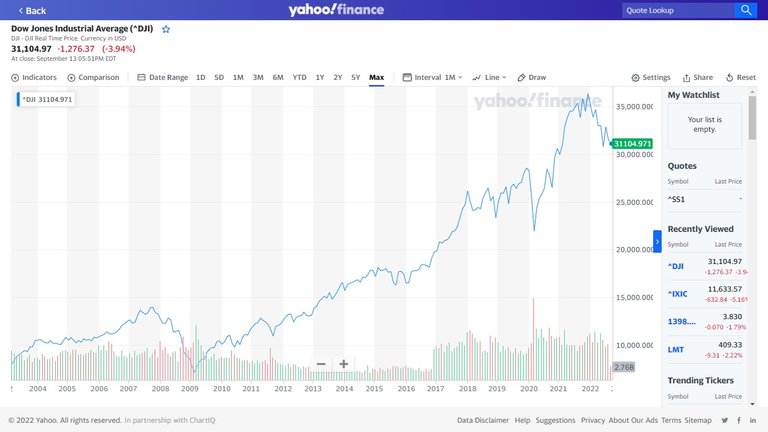

Figure 9 contains the Dow Jones Industrial Index (stock market index of 30 prominent companies listed on stock exchanges in the USA) between 2003 and September 2022.

Figure 9: Dow Jones Industrial Index

Source: Yahoo Finance

The index shows that the largest companies often experience a sharp dip in share price at the beginning of the economic downturn but recover quite quickly compared to the rest of the economy. This was particularly true during the Covid-19 response period and will likely follow through in the second half of the crisis. Falling share prices do not always indicate that businesses are entering financial difficulty. Some investors sell out of panic. This an opportunity for other investors to make a quick return. Hence, the quick recovery. Prices would remain low considerably longer if these businesses were in any significant financial trouble.

Banks

It is intuitive to believe that banks will perform badly during an economic crisis. People and businesses are more likely to default on their loans. Other investments are more likely to fall in value. Left purely to free markets forces, banks would struggle if they were not financially prudent. However, banks are not purely at the mercy of markets when the economy crashes. The 2008 to 2010 financial crisis is a perfect example of big banks escaping the consequences of their actions.

The 2008 to 2010 financial crisis was triggered by banks profiting from lending money to people who could not sustainably make repayments in the longer run. They offered mortgagees with minimal down payment requirements to lure more people into the housing market. This caused house prices to continuously climb. People were willing to buy with a small down payment because they could not afford a larger down payment or because they were enticed by the increasing house prices as a form of investment. Eventually, the number of people defaulting on loans, mortgages in particular, began to climb. House prices began to plummet. For many, the amount owed on the mortgage exceeded the price of the house they bought (CNN Money). This reduced people’s incentive to continue making repayments. Many banks were likely to face financial ruin. Several banks went bankrupt, Lehman Brothers being the most notable bankruptcy.

Other major banks were not at risk of failure because the Government bailed them out. In 2008 and 2009, over $200 Billion was distributed by the US Treasury to the banking sector. Approximately US$90 Billion went to just four banks (Wells Fargo, Bank of America, JP Morgan Chase, and Citigroup) (CNN Money). Over a decade later, many banks have still not paid back the amount in full. The bailout approach was not unique to the USA. The UK Government adopted a similar approach, which involved a £137 Billion package to save the banks (UK Parliament).

The bailouts enabled the bigger banks to take advantage of low cost investment opportunities such as buying other struggling businesses (Jonathan Turley). The financial companies that went bankrupt or partially failed were being bought by the ones that had been bailed out (Wikipedia). Bigger banks became even bigger despite taking risks that should have bankrupt them.

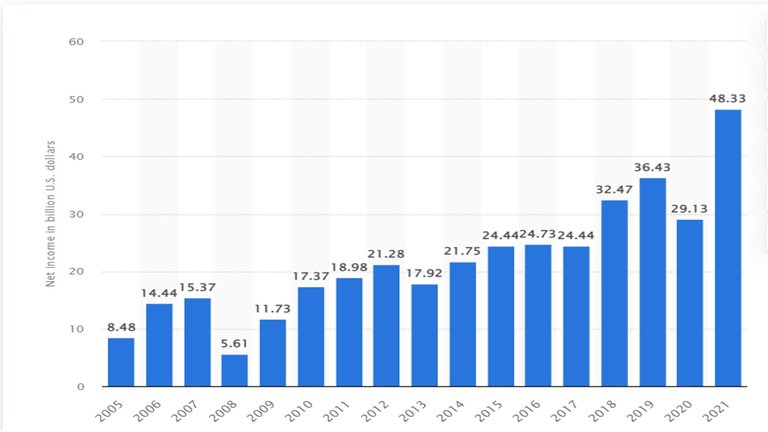

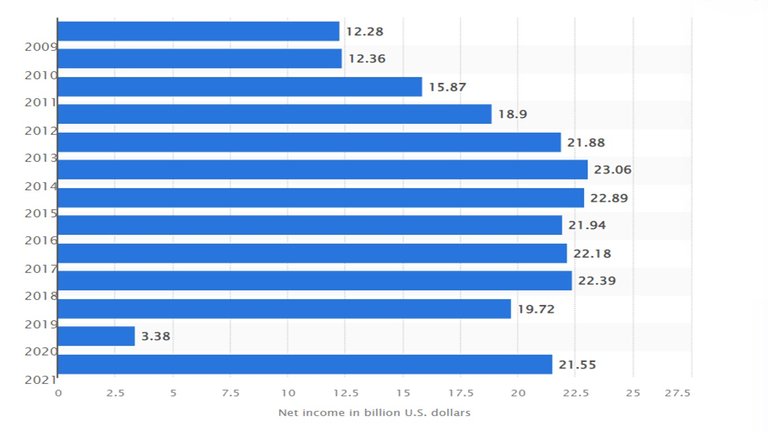

Since the financial crisis, the biggest US banks such as JP Morgan Chase, Bank of America, Citigroup, and Fargo Wells have performed well. See Figures 10, 11, 12 and 13.

Figure 10: Net Income for JP Morgan Chase (2005 to 2021)

Source: Statista

Figure 11: Net Income for Bank of America (2009 to 2021)

Source: Statista

Figure 12: Net Income for Citigroup (2005 to 2021)

Source: Statista

Figure 13: Net Income for Fargo Wells (2009 to 2021)

Source: Statista

The risk to the banks during the “Cost of Living Crisis” will be less than during the financial crisis as they are not at the centre of it. Even if the banks are at risk, they have little to worry about. Even though, they are unlikely to be bailed out. Instead, there would be bail ins. Banks will be able to use their customers deposits as their own equity to help themselves financially (Investopedia). Instead of receiving taxpayer money, they will be allowed to steal from their customers. Like with previous economic crises, there will be plenty of opportunities to create more loans and acquire struggling businesses, which will enable banks to reap huge profits once the economy is booming again.

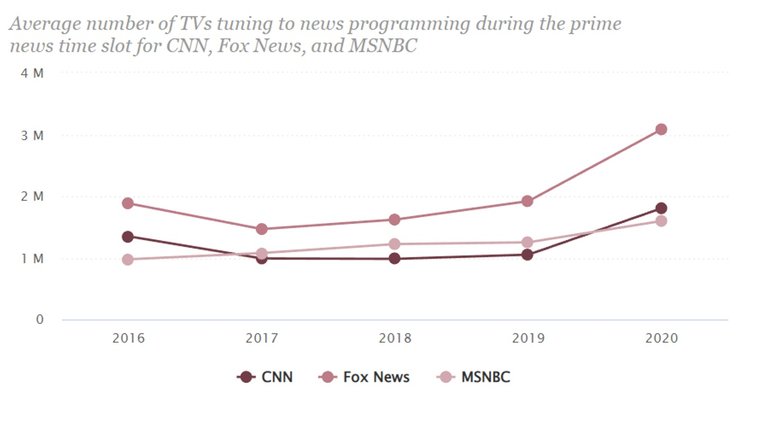

Media

News media gain attention through interesting, exciting, and supposedly important news stories. For example, pandemics, wars, social unrest, and economic crises. The past three years has had all these events. Figure 14 contains the average number of viewers watching the three largest News Networks in the USA.

Figure 14: Viewership for Fox News, CBB, and MSNBC (2016 to 2020)

Source: Pew Research Center

News networks in the UK are also experiencing growth in viewership since the beginning of the Covid-19 fiasco. Below are examples of the growth in audience from 2019 to 2020.

- BBC reached a weekly audience of over 20 million across its evening bulletins of 6pm and 10pm.

- BBC.com had its largest audience ever in March 2020.

- ITV Evening News viewership is up a fifth.

- In 2020, Channel 4’s viewership was up three times what it was in 2019.

- Sky News had its highest viewership since 2011.

Source: Press Gazette

The media are an essential propaganda resource for the Establishment. High viewership is good for promoting Establishment ideology and fearmongering so that people are more receptive to the ideology. Normally during a crisis there is more propaganda, as Governments want scapegoats for the crisis as well as promote the actions they are proposing. Media serves to either support and promote proposed Government action or oppose it by demanding that the Government does more to directly combat the crisis. This influences people into thinking the Government needs to be doing more (i.e. more intervention). The media usually fails to adequately discuss the true causes of the crisis, which, in most cases, is a result of previous or even current Government actions.

Religion

In my post The Old Gods and the New, I discussed the growth in religion around the world. Despite many people turning away from religion, the number of people who follow a religion is still increasing. This is because religious people tend to have more children. Therefore, religion remains an integral part of most societies.

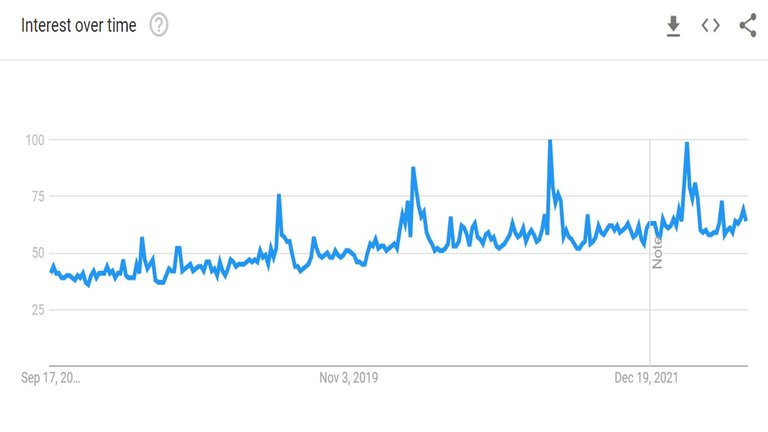

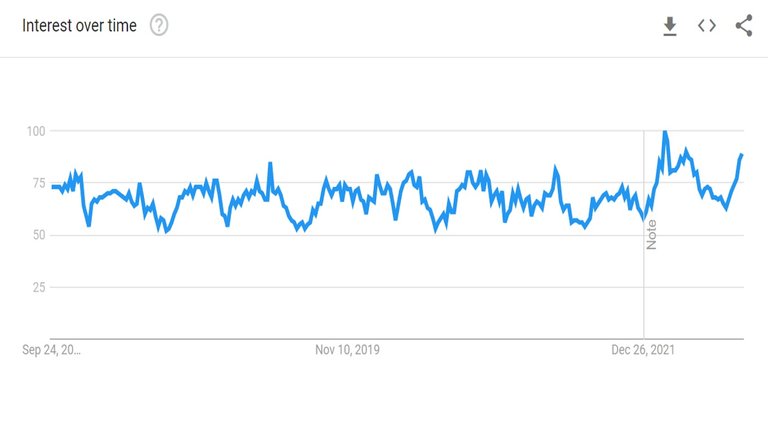

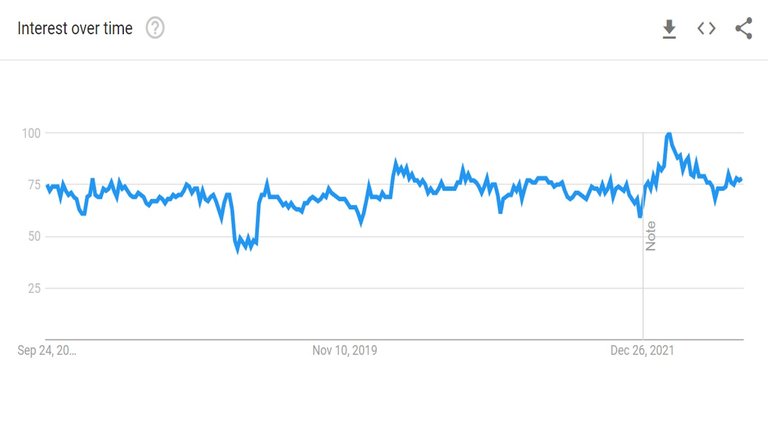

During hard times people to turn to religion for comfort and reassurance. During the Covid-19 fiasco, restrictions prevented most people from attending religious services. Therefore, it was not as easy for people to turn to religion. Despite the restrictions, people appear to still be turning to religion. According to Google Trends, several key words and topics relating to religion have higher search numbers worldwide over the past few years. These include prayer, religion and faith (topic).

Figure 15: Google Trends Prayer

Source: Google Trends

Figure 16: Google Trends Religion

Source: Google Trends

Figure 17: Google Trends Faith (Topic)

Source: Google Trends

Now that restrictions have been lifted in most countries, it is likely that attendances at places of worship will increase as the “Cost of Living Crisis” worsens. However, it may still remain below pre-Covid-19 levels as people have discovered how to practice religion from their homes instead of attending services (Web Tribunal). Therefore, actual numbers of people turning to religion will be difficult to determine.

US Establishment

The US Establishment have had an interesting past few years. They implemented strict restrictions in response to Covid-19 (some States more so than others). They had months of Black Lives Matter (BLM) protests and riots triggered by the killing of African American man George Floyd. In early 2021, they had a controversial change of President (media and social media manipulation of information regarding candidates as well as anomalies in vote counting). In the same year, they had an embarrassing military withdrawal (defeat) from Afghanistan. Their support of Ukraine has drained their country of billions of dollars and a large amount of military equipment which will be replaced. Sanctions on Russia have triggered highest inflation in decades. However, most of this inflation was caused by the massive increase in money supply in 2020. All of this has been bad for the US

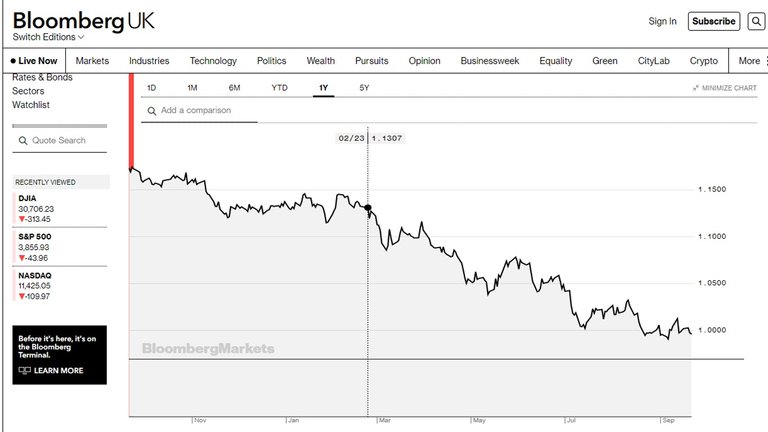

The US Establishment may end up as winners from the “Cost of Living Crisis”. Europe is suffering far worse from the effect of sanctions on Russia than the USA. This is because most countries in the European Union (EU) have a far greater dependence on Russian energy than the USA. For example, in 2020, Russia supplied Germany, largest country in the EU, with approximately US$6.38 Billion worth of crude petroleum (1/3 of its imports) (OEC World) but only supplied the USA with US$979 Billion worth (1% of its imports) (OEC World). An early indication of this advantage is the rapidly strengthening US dollar against the Euro over the course of the war in Ukraine so far. See Figure 18 below.

Figure 18: US dollar against the Euro (September 2021 to September 2022)

Source: Bloomberg

If the economies of the EU collapses, they might be forced to become dependent on the USA to meet many of its needs. This would strength the US economy but even more significantly, it would strengthen it politically on the world stage. This will become more evident once the crisis ends. China is also likely to benefit in a similar manner (discussed in the next section).

A partially leaked report (Executive Summary only) from RAND Corporation (company that provides research and analysis services to the US Government) outlines a plan to disrupt Russia’s supply of oil and gas to Germany in an attempt to weaken the German and European Union economies. The destruction of a major competitor could be a great benefit to the US Establishment. It is likely to cause capital and skilled workers to flow from Europe into the USA. This report can be accessed on Weltexpress and Red Pill News websites.

I believe the leaked report to be genuine. The arguments constructed in the report appear logical and consistent with the events that are occurring. For examples, the push for strict sanctions (particularly around energy), unwillingness to encourage peace talks, mainstream media propaganda and highly selective reporting, and the excessive provision of weapons to the Ukraine.

The EU citizens are going to suffer significantly during this “Cost of Living Crisis”. The EU establishment will make up for their loss of significance on the world stage by gaining power in Europe. Many European countries outside the EU will be affected as badly if not worse than those in the EU. Their leaders will use that as an excuse to join the EU. The EU will lower their standards just to have a larger membership. As of 2022, the EU has 7 candidate countries wanting to join the EU (Albania, Moldova, North Macedonia, Montenegro, Serbia, Turkey, and Ukraine) (European Comission).

China’s Establishment

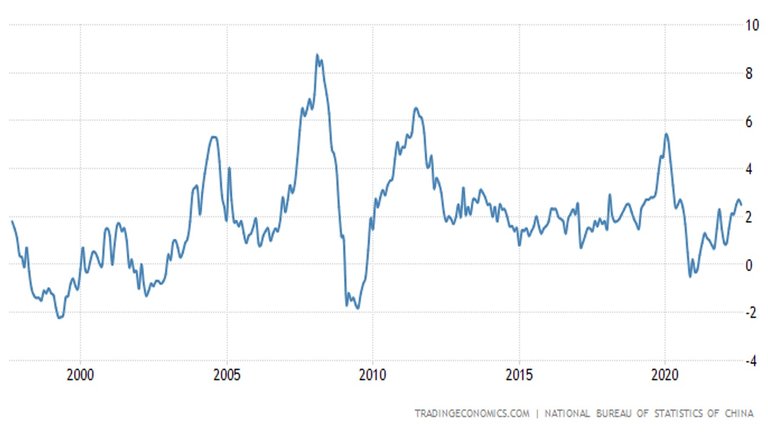

It does not appear that China has been pulled into the “Cost of Living Crisis” to the same extent as the European countries. They have not attacked Russia with sanctions nor sent money to Ukraine. They are implementing a disastrous zero Covid-19 policy. This policy has significantly stunted their economic growth. However, they can easily put their economy back on the path to recovery. China does not suffer from high inflation; see Figure 19.

Figure 19: Inflation Trends in the China (1997 – 2022)

Source: Trading Economics

The green agenda stands to greatly benefit from the increasing cost of energy. Green options are becoming relatively cheaper. China has some of the largest Lithium mining companies in the world (Jiangxi Ganfeng Lithium Co. Ltd and Tianqi Lithium with market caps of US$38.6 BIllion and US$24.39 Billion respectively as of 2021 (Mining Technology)). Chinese electric vehicles are rapidly gaining a strong foothold in European car markets. In Europe, in 2019, they had 0.5% market share of the electric car market. In the first quarter of 2022 that has increased to 18.7% behind only Germany (Inside EVs). Chinese companies are also dominating solar panel markets and wind turbine markets. As of 2022, eight of the top ten solar companies (Energy Sage) and six of the top ten wind turbine companies in the world are based in China (Biz Vibe).

Global Establishment

The Global Establishment is the combination of world’s largest countries Establishments. The World Economic Forum (WEF) have outlined their strong desire for greater centralisation of power in their Great Reset and Fourth Industrial Revolution strategic plans. This would involve decisions being made global by a few different organisations consisting of leaders from the biggest and most powerful countries. This is likely to be a combination of politicians, business leaders, bankers, and any other global elites. Their aim will be to tackle global problems. I would expect them to frame most problems as being global to at least a certain extent so as to extend their power as far as possible. My posts My summary and opinions regarding ‘The Great Reset’ – Part 6: Conclusion and A Peripheral look at the Great Reset and Fourth Industrial Revolution contain more in-depth discussions about WEF and their agendas.

Much of what the Global Establishment are planning is already in motion. This has been demonstrated by the responses to Covid-19 as well as the Ukraine war. There is considerable control being exerted on a global level. However, this is not completely or consistently unified at this point. Neither does it have sufficient support from the publics of most countries. Significant change is still required for this global agenda to have a complete grip on the world. The only way this might be possible is if the world collapses. This will involve both social and economic collapses. It needs to be so bad that people will become desperate for a solution to end their hardship. The current “Cost of Living Crisis” is another stage in this collapse. It is unlikely to be the last stage.

Losers

The majority of the world will be losers as a result of the “Cost of Living Crisis”. This crisis is likely to negatively affect more people than any other crisis that has come before it. It is a combination of health, energy, food, and cost crises rolled into one. It will affect every country and every continent. For example, most African countries were barely affected by Covid-19 nor involved in the Ukraine-Russia war but they could be worst hit by this crisis. Many African countries may face famine because of food shortages caused by disruption in supply chains, drought, deliberate destruction of food, and reduced support from wealthier countries.

I believe one of the biggest losers in western countries will be small businesses and the self-employed. They were greatly affected by the Covid-19 restrictions and the increased costs of running their businesses triggered by sanctions on Russia and excessive increase in money supply. They are also often the most affected during a recession as demand falls. The “Cost of Living Crisis” will affect them on both the demand and supply sides. Many will be too vulnerable to survive.

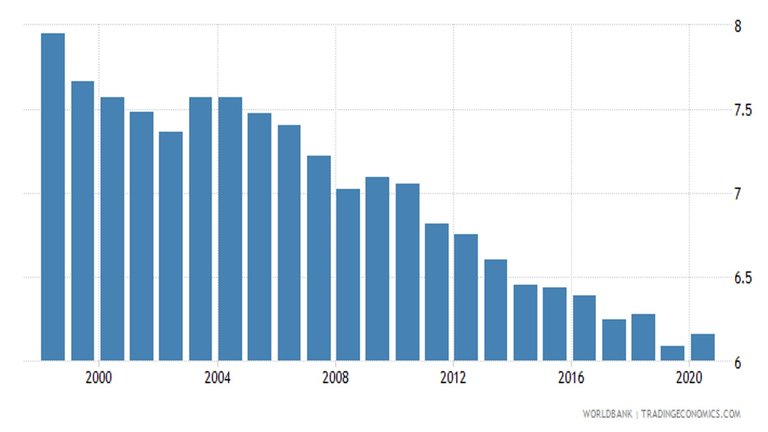

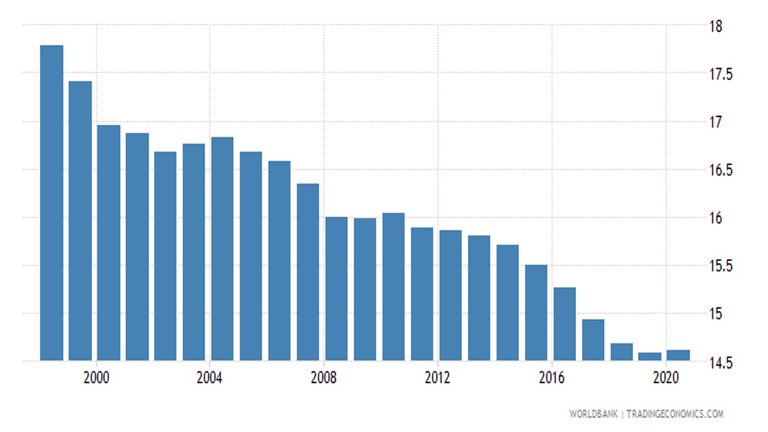

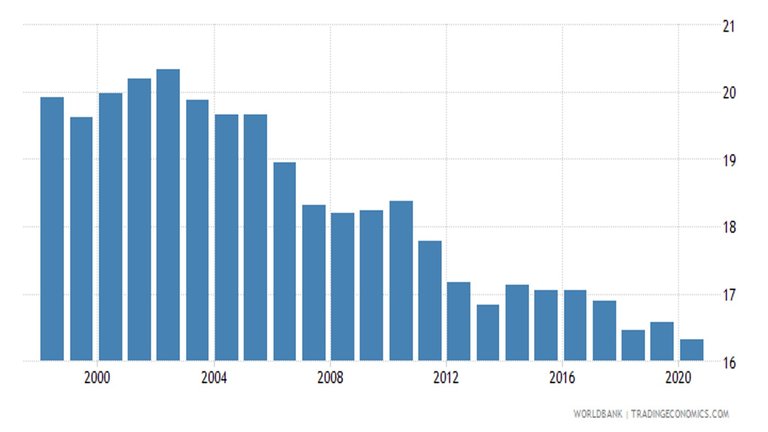

Figures 20, 21, 22, and 23 contain the percentage of self-employed people in the USA, UK, Euro Zone, and Australia.

Figure 20: Self-employment in the USA (1998 to 2021)

Source: Trading Economics

Figure 21: Self-employment in the UK (1998 to 2021)

Source: Trading Economics

Figure 22: Self-employment in the Euro Zone (1998 to 2021)

Source: Trading Economics

Figure 23: Self-employment in the Australia (1998 to 2021)

Source: Trading Economics

With the exception of the UK, the number of self-employed people as a percentage of the workforce has been continuously falling for over two decades. The “Cost of Living Crisis” can be expected to lower these percentage further as employment shifts to Big Business and possibly to Government jobs.

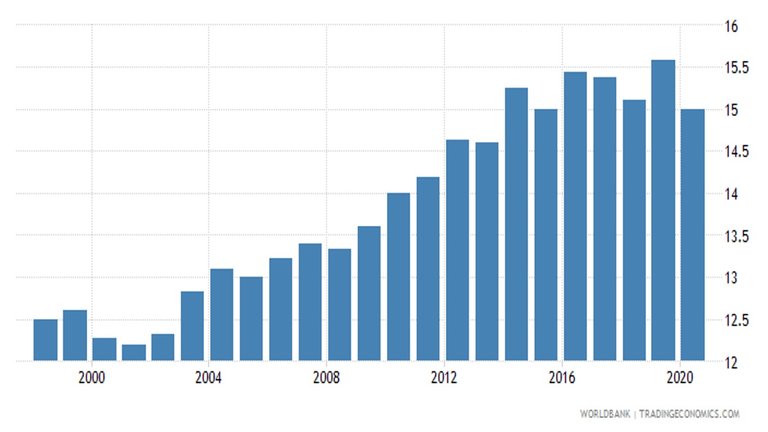

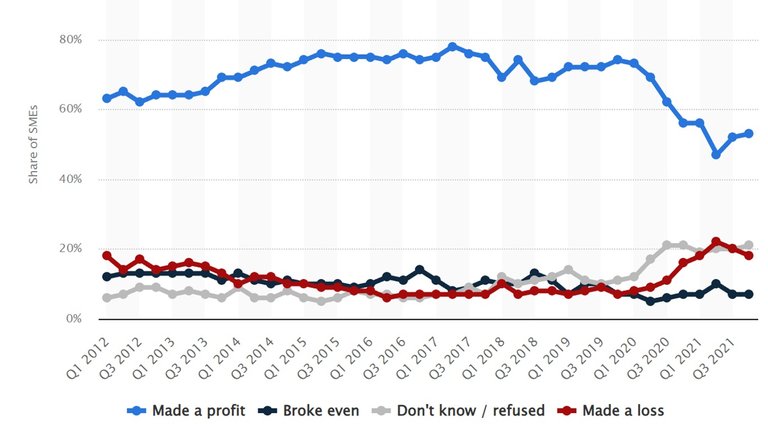

For most countries, recent data has been difficult to acquire in regards to performance of small and medium businesses. For this post, I have only included data for the UK. Figure 24 contains this data for the first quarter of 2012 to the first quarter of 2022.

Figure 24: Profits for small businesses in the UK (first quarter of 2012 to the first quarter of 2022)

Source: Statista

Profits declined sharply when harsh Covid-19 restrictions were applied in the UK. When restrictions were relaxed in 2021, profits continued to fall. Even after the removal of restrictions, profits are well below pre-Covid-19 levels. These figures do not include the impact of the increasing costs from the second quarter of 2022 onwards. This is a troubling sign for small and medium businesses. I expect the small and medium businesses in the Euro Zone, which are facing similar circumstances to be struggling to a similar extent.

The elderly are another group of people who could be greatly affected by the “Cost of Living Crisis”. The elderly rely on savings and pensions to survive. High inflation will greatly reduce both their spending power and the savings they have accumulated over their careers. For many countries, Covid-19 responses has created a health crisis (e.g. shortages of medical staff and wasted money on "vaccines"). Elderly tend to require more healthcare because of their age. The elderly are also more affected by cold weather. The very high costs of energy could mean many elderly people will not be able to sufficiently heat their homes this winter. The “Cost of Living Crisis” is bad for most groups of people but the elderly have the highest risk of dying because of it.

Wrapping it up

The “Cost of Living Crisis” might be the most manipulated crisis in history. It began with decades of suppression of people’s incomes. Standard of living only improved with the accumulation of household debt. Productivity has continued to grow but the rewards of such gains have been almost entirely adsorbed by the wealthiest in society (see my post Cost of Living Crisis – A Collection of Symptoms caused by Serious Long-term Political Failure for a detail explanation).

The crisis was first triggered by the strict and almost global response to Covid-19. Lockdowns shut major cities down completely for weeks and in some cases months. This was followed by restrictions, which still greatly prevented normal activity from resuming. During this period, Governments handed out billions of dollars, pounds, euros, etc. to people and businesses who were prevented from earning an income. Most of this money came out of nowhere. Forced reduction in economic activity plus drastically increased money supply was going to inevitably lead to stagflation.

The crisis was further triggered by the war in Ukraine and the responses that followed. The war in Ukraine appears staged by US and Ukraine provocation as well as Russia’s aggressive response. Once the war began US and all of its allies immediately responded with sanctions and in some cases theft of property. Some of these sanctions targeted energy supplies to Europe; thus, causing energy prices to rise rapidly. The flooding of Ukraine with weapons served to extend the war as long as possible and if you believe the leaked RAND Report, it intended to cause as much economic harm as possible to the people of the EU.

The “Cost of Living Crisis” from the start has been orchestrated by Government intervention. Most of the winners have been guided by intervention. Most of the losers have been trapped for a long time. Ironically, the solutions that are being most vocally demanded for involve yet more Government intervention. This is because most people will struggle to survive this winter without some form of help. Governments have successfully made many people dependent on them. The “Cost of Living Crisis” is likely to benefit almost every part of the Establishment. The major role Governments have played makes them the biggest winners of all.

More posts

If you want to read any of my other posts, you can click on the links below. These links will lead you to posts containing my collection of works. These 'Collection of Works' posts have been updated to contain links to the Hive versions of my posts.

Hive: Future of Social Media

Spectrumecons on the Hive blockchain

Excellent presentation and articulation of data and facts. The only way that you gain a realistic handle on what is currently taking place in the economy, and subsequently the market, is to dive in and consume the data. Again, excellent content!

Posted Using LeoFinance Beta

Thanks @sapphirecrypto. There is quite a bit of data out there but it involves quite a bit of digging. In most cases, the most recent data is not available but what is available offers strong indications of where we are and where we are likely to be heading.

This post has been manually curated by @steemflow from Indiaunited community. Join us on our Discord Server.

Do you know that you can earn a passive income by delegating to @indiaunited. We share 100 % of the curation rewards with the delegators.

Here are some handy links for delegations: 100HP, 250HP, 500HP, 1000HP.

Read our latest announcement post to get more information.

Please contribute to the community by upvoting this comment and posts made by @indiaunited.

One thing I have come to realise is most of the time when there is an economic crises, the government does not tend to lose as the people or should I say citizens. The citizens tend to suffer more of the effect on their side during economic crises

It depends on the nature of the crisis. In the context of this crisis, the average citizen is going to be badly effected. Even those who have prepared themselves are not going to have it easy. People who haven't prepared themselves are heading into a nightmare.

Many people don’t know recession is part of everything and even in our day to day life’s we sometimes where things won’t be going as planned but we have to keep pushing. During recession what is important is finding a way to survive without destroying our investment.

Government intervention are very important in making out of recession but that’s it is the right intervention like the one you have stated in this paragraph because interest rate is increasing on daily bases in U.S now which positive impact does that have on the present economy situation?

Most of the major companies listed above are doing amazingly during this time and will continue to do well especially the pharmaceuticals and weapons companies.

I always thought banks are the problems because of what happened in 2008 and now things are different in many ways, not Covid 19 that caused this recession it is the mismanagement of the economy.

Conclusion

Government intervention for this recession has not been enough and they are not helping matters looking like they are trying to support the pocket of the banks. I hope this doesn't take longer than expected.

Posted Using LeoFinance Beta

Most recessions are challenging but they also offer opportunities to people who can recognise them and have positioned themselves to take advantage of them. It is like a crypto bear market. There are opportunities to accumulate assets that will appreciate in price when the market picks up, which it does eventually.

Intervention during a recession is typically expansionary policy; this stimulates activity (i.e. increases demand). However, expansionary policy is inflationary. This does not normally matter as inflation is normally low during a recession. This time it is different. Growth is low and inflation is high. They cannot both be tackled at the same time using demand side policies.

Increasing interest rates is contractionary policy that is used to reduce inflation. This slows the economy down. Under current circumstances, it will make a recession worse. The causes of the crisis need to be addressed. They are mostly on the supply-side and caused by past interventions. Sadly, it is going to take a long time to fix.

I consider Covid-19 policies as a trigger. They were very damaging but this has been because economies have become very vulnerable. If Covid-19 had never happened, something else would have triggered this current crisis.

Excellent if somewhat depressing post.

You spoke about the long-term effect of recession. Now you highlighted that it might be good because it Makes government and people adjusts their actions and cultivate better policies right? Now the question is, if series of recession is left uncheck, would the natural process of recovery be adequate enough to prevent another recession? Because you talked about it majorly caused by bad policies. Should we say constant recession prevents a country from getting to a stage of recession where it might be difficult for them to recover?

The crony capitalism you're speaking of isn't it a kind of situation where big pharms enjoy the benefit of government policies, while paying it forward in forms of tax?

Well, you've rightly said the demand for healthcare is inelastic, I'm thinking, the current COVID-19 situation in the world might just increase that inelasticity, creating a sort of situation where wealth would be massively generated to companies who are providing them, right?

Now, Theoritically, if the cost of e crises were to affect everyone in general, organizations and people alike. do you think it'll be a good thing?

This has been very insightful..

@tipu curate

Upvoted 👌 (Mana: 40/50) Liquid rewards.

This is my first time of commenting here on your post sir although am a nursing mom. I have something to say as well on this economy Crisis and co. Hmmm. I will say that categorically speaking any world of economy inflation due to bad economy management and restructuring will take more than long term to meet the demands of the masses. Take for instance, here in Nigeria is a case study where we have so many resources but we misused them all and yet we are going from one unstable economy to another. @spectrumecons I followed you.

This Crisis is a pain in the ass! hope for recovery